Business of Uncertainties: An Afflict of COVID-19 on Indian Insurance

Anjali and Geeta Arora*

Department of Mathematics, Lovely Professional University, Phagwara, India

Email.id: anjalimeets@gmail.com; geetadma@gmail.com; geeta.18820@lpu.co.in

*Corresponding Author

Received 09 June 2021; Accepted 05 August 2021; Publication 17 September 2021

Abstract

COVID-19 had far-reaching consequences for different economic sectors around the world. While the impact was not standardised throughout, one thing was consistent: every sector and region, including India and the Indian insurance sector, faced challenges in adapting to the new normal. The insurance industry provided both life and non-life or general insurance. COVID-19 had a mixed effect on the insurance industry. The effect of COVID-19 on the insurance industry was not uniform; some products saw a significant increase in business, while others saw a significant decrease. The aim of this research is to examine and assess the overall effect of COVID-19 on the insurance industry with emphasis on the steps to be taken to prepare the insurance sector to deal with these types of the consequences in the future. Data from the regulatory authority’s website is used to compile and analyse the findings of the study.

Keywords: COVID-19, insurance, economy, health insurance, business.

1 Introduction

COVID-19, an acronym for novel CORONAVIRUS disease, is an influential force that demonstrates the sudden and unforeseen blow in various spheres of society. With the first case in December 2019 in Wuhan, China, the virus quickly spread all over the world in just a few months. It has infected 41.3 million people worldwide, including 7.71 million in India alone, and the number is still fluctuating with millions of people being vaccinated and recovered ((COVID-19), 2020). COVID-19 was declared as a global pandemic by the World Health (Director-General, 2020), which is a viral disease that has not only affected humans, but also has a negative effect on the country’s economy.

The nationwide lockdown in India from March 24, 2020 shortly after COVID-19 being declared as a pandemic had a negative effect on the Indian economy because development activities were fully halted during the lockdown. India is one of 15 countries whose GDP was negatively affected. According to a report released by the Ministry of Finance, India’s GDP rate fell to its lowest level ever after this lock down. Its GDP drops from 4.5% in the first quarter of FY19 to 23.9% in the first quarter of FY20 (ET, 2020). According to the survey, India’s life insurance firms have grown their business by 11.36% by the end of March 2020. In FY20, the insurance industry grew by 13% for non-life insurance while 18% for life insurance (Brand India, 2020).

Indian Insurance Industry: Insurance is a method of transferring a person’s risk of physical assets and life to insurance providers in exchange for a premium. In exchange, insurance providers agree to pay for any losses incurred by the insured (the person who applies for insurance protection). The Insurance Regulatory and Development Authority (IRDA) in India is governed by an Act of Parliament, the Insurance Regulatory and Development Authority Act, 1999, which regulates and supervises the insurance industry (IRDAI Act 1999). The Authority has the rights to enact a variety of legislation, ranging from the registration of insurance companies to the safety of policyholders.

There are two kinds of insurance policies: one is life insurance, which covers human lives and pays only until death or the maturity of the policy. On the other hand, general insurance, also known as non-life insurance covers fire, health, motor, marine, engineering, and other miscellaneous risks, and reimburses policyholders for damages incurred during the policy duration.

Growth of Indian Insurance Industry: The insurance industry in India is a massive industry that is expanding at a rapid pace of 15-20% each year (IRDA, 2020). Insurance and banking services together account for approximately 7% of the country’s GDP (IRDA, 2020). A fully functional insurance sector is beneficial to economic growth because it provides long-term funds for infrastructure development while also increasing the country’s risk-carrying ability. It is the foundation of every industry since it operates on the basis of risks and promises. The essence of the insurance industry is such that a significant incident today has a long-term effect on the industry. Many individuals who have never purchased insurance are now showing their interest in this direction and will continue to do so for the remainder of their lives. Human health, as well as the various other sectors become at risk and uncertain during this pandemic. As a result, people would undoubtedly need the assistance of an insurance provider during this trying time.

The work in this paper is based on the discussion on entire insurance industry, with a particular emphasis on the health insurance sector. Various growth and accretion trends among various companies and tycoons are discussed in this paper. Since the insurance industry is focused on risks and obligations, and COVID-19 has affected both, that makes the need to explore this effect. In terms of business growth, the pre-covid period is also compared to the post-covid period (Monthly Business – Life, 2020) (Industry Performance, 2020). The analysis also looks at how the insurance industry dealt with these risks and met the insurer’s demands.

2 COVID-19 as a Global Pandemic

The novel coronavirus has spread through 200 countries and territories. There are 158 million confirmed cases and 3.29 million death cases, with more on the way ((COVID-19), 2020). The key cause of this illness is the severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2), a highly infectious flu strain. From the first recorded case in China’s Wuhan city to the spread of the virus to every other country on the planet, it has been the world’s worst crisis. The WHO changed COVID-19’s status from Public Health Emergency to Global Pandemic in just 42 days. COVID-19 pandemics are uncommon, but their influence has been felt for a long time. Around 170 countries had the lowest GDP per capita at the end of 2020, resulting in a global economic contraction. According to the study, G20 economies have shrunk by 3.4% year on year, with about 400 million full-time jobs lost, about US$3.5 trillion in lost income for people worldwide (Winck, 2020), and global economic growth estimated at 4.9% contraction in 2020 (IMF, 2020). The covid-19 pandemic has left scars all over the world, with approximately one-third of the population trapped in their homes, resulting in an economic downturn, diminished well-being, and lost employment.

3 COVID-19 and Its Impact on India’s Economy

Following WHO declaration of COVID-19 as a pandemic on March 11, 2020, India implemented its first Janata Curfew on March 22nd, followed by another on March 24th. The main goal of the curfew was to prevent coronavirus from spreading. Following that, on March 25th, 2020, Prime Minister of India announced the start of the first period of lockdown, which would last for 21 days (Wikipedia, 2020). The government of India has extended the complete lockdown in four phases, keeping an eye on COVID-19 cases and their impact across the world. After 75 days of lockdown, the process of unlocking began, with just 606 cases and 10 deaths at the start of the lockdown rising to 2,50,000 COVID-19 cases and 7200 deaths. India has now become the world’s second most affected region, with 10.5 million confirmed cases and 1.5 million deaths (Kumar, 2020).

The effects of 75 days of total lockdown on society and its inhabitants have been recorded. Thousands of people were forced to flee from India’s major cities after discovering that they were jobless. About 140 million people lost their jobs, and many more had their salaries reduced. It obstructs the functioning of common workplaces and services such as transportation, educational institutions, industrial works, hospitality, and manufacturing services, all of which have impacted India’s economic situation.

According to data released by the National Statistics Office, India’s GDP levels fell to its lowest level in four decades. Its GDP falls from 4.5% in the first quarter of FY19 to 23.9% in the first quarter of FY20. Construction is at 50.3%, Trade and Hotels is at 47%, Manufacturing is at 39.3%, Industries is at 38.1%, Mining is at 23.3%, Services is at 20.6%, Public Administration is at 10.3%, Power and Gas is at 7%, and Agriculture is at 3.4% in Q1 (ET, 2020). Even though every sector is experiencing negative growth, India’s life insurance companies saw an increase of 11.36% in business at the end of March 2020. In FY20, the insurance industry grew by 13% for non-life insurance and 18% for life insurance (IBEF, 2020). Following the unlocking of the lockdown process, there was a slight improvement in the Q2 GDP rate. India’s economic growth has slowed from 23.9% in Q1 to 7.5% in Q2 (Web-Desk, 2020). India’s economy has entered a technical recession as a result of these two successive negative growth rates. COVID-19 is not only a viral disease that affects humans; it has also had an economic impact on the world.

3.1 Manufacturing Sector

Any country’s growth and development are reliant on its manufacturing sector. It is important for both developed and developing countries to grow economically. It is a facility that develops and processes new technology and goods. The manufacturing sector in India grew at the fastest pace. Many large corporations have been invited to set up in India as part of Indian Prime Minister Narendra Modi’s “Make in India” initiative, which aims to make India a global manufacturing hub on the world map. Manufacturing contributes 16–17%t to GDP and employs roughly 12% of the workforce (CII, 2020). COVID-19 has disrupted the product’s supply chain, affecting the manufacturing industry. In Q1 of FY20, lockdown had the most negative impact on the market, with a contraction of 39.3%. In Q2, the manufacturing sector rebounded to 0.6% expansion, turning India’s economy in the second quarter (Dhoot, 2020). And it is because of this positive growth in the Indian manufacturing sector that the present exists. And it is because of this positive development in the Indian manufacturing industry that the current situation has emerged, in which the pandemic has turned out to be a blessing in disguise for the industry.

3.2 Service Sector

India’s service sector accounts for 57% of the country’s GDP. Trade, transportation, banking, insurance, real estate, business services, community, hotel and restaurant services, storage and communication, social and personal services, and construction services are all included. As a result, it is a critical component of India’s economic growth (IBEF, Brand India, 2020). The government has enforced lockdown, restricting all facilities that have affected the world, in order to curtail or eradicate the virus outbreak. As the most competitive market, travel and tourism has lost 40 million direct and indirect jobs, as well as a USD 17 billion annual revenue loss due to a 66.4% drop in overseas tourists in March 2020 (Jaipuria, Parida, & Ray, 2020). On a year-over-year basis, India’s airport authority announced a 92% drop in aviation business (Mallapur, 2020). Construction witnessed 50.3% decline, power and utility services slipped by 7%, hostel, trade, transport, communication, and broadcasting services contracted by 47%, the only agriculture sector has a growth of 3.4% in Q1 of FY20 (ET, 2020). The impact on the service sector was still the same in Q2 as reported in Q1, hence, the services sector still facing the worst hit.

Some industries, such as IT, finance, e-commerce, and education, have been able to operate their businesses or properties using new normal methods. Allowing workers to work from home with a minor pay cut has proven to be a more effective way of running a company and being relatable throughout the pandemic. The unexpected pandemic, followed by an unanticipated lockdown, put corporations’ Business Continuity Planning (BCP) to the test, making BCP an important investment for the organisation. Despite the lockdown, some industries continue to provide services by encouraging their workers to operate from home. In such a short time, shifting from a traditional market to a purely digital market has aided the country and its citizens in surviving the pandemic and securing their future growth. A pandemic is unavoidable but providing a good BCP with risk reduction capabilities would ensure that the economy runs smoothly.

3.3 Insurance Sector

The insurance industry is one of the most important sectors in the economy, accounting for around 5% to 7% of GDP. Several changes occur in every field of the economy during this pandemic. With the reported rise in business in the health insurance sector, the insurance sector as a whole is experiencing a downturn. In India, only 18% of the population in urban areas and 14% of the population in rural areas have health insurance.

The effect of COVID-19 on the insurance industry is addressed in a report by Babuna et al. (Babuna et al., 2020), which uses the case study of the Ghanaian insurance industry during the COVID-19 as a case study. According to the author, until June 2020, Ghana has reported 14,007 confirmed cases of novel coronavirus. Ghana’s president placed a partial lockout in March 2020, but it was lifted in April 2020 due to the country’s impending economic collapse. A monetary loss of GH₡ 112 million has been suffered by the Ghana insurance industry. However, instead of a financial loss, it shows some unexpected business development. The annual profit has dropped by 16.6% as the overall premium has dropped by 17.01%, while client claims have increased by 38.4%. Insurance plays a major role in Ghana’s economy. It suffers from a severe lack of infrastructure, necessitating the creation of effective insurance policies in order to pursue economic growth. The authors have proposed several actions to reduce the impact of a pandemic on morbidity, mortality, and social disruption, based on the authors’ observations of the Ghanaian economy and insurance industry.

Another study is conducted by Shekhar on the effect of COVID-19 on the insurance sector and the transition to a new normal existence in the wake of the pandemic (Shekhar & Pandey, 2020).This research aims to assess the impact of COVID-19 on all major stakeholders, including hospitals, insurers, and corporations, as well as the impact of COVID-19 on constantly evolving claim trends, various protective models, and digitalization modes. It proposes several strategies for reducing confusion and preparing for future digital shifts. The authors have addressed the impact of insurance claims made on insurers as a result of the high cost of COVID-19 positive care, which has resulted in a decrease in the number of patients seeking cancer, dialysis, and maternity treatment, both of which have seen a significant drop in post-lockdown.

Another research, conducted by Jaydeep Joy of PwC India, is a report on the effect of COVID-19 on the Indian insurance industry (Roy, 2020). After consulting with top chief financial officers (CFOs), the report was produced. To protect homes, properties, and businesses, we all need the services of the insurance industry. Life insurance covers people’s livelihoods, future incomes, businesses, and net worth, while general insurance covers a company’s assets and economic activities. According to the survey, 51% of CFOs anticipate a decrease in revenue collection of up to 25% and a 26% decrease in profit received by businesses as a result of COVID-19. Liquidity, portfolio risk, amount of free assets, dependency on reinsurance, and reinsurance cover were all changed in various ways on insurance companies. Some protocols for handling and qualifying damages suffered during the pandemic are being recommended again. One of these practices is for the insurer to act quickly in order to gain the client’s interest. Insurance firms should keep an eye on the cause-and-effect chain, global activities, and market dynamics. To prevent risks, the company should obtain expert advice early on, and it must consider the drivers of the insured’s business model.

4 Data and Methodology

4.1 Data

Data for the study has been taken from the Indian Insurance Regulatory Authority of India and General Insurance Council of India websites. The data contains the segment-wise business figure of the general insurance sector. The data and reports from the World Health Organization, Ministry of Health, Ministry of Finance, and National Sample Survey of India have also been considered for the study. COVID19 case updates and information about pandemic response around the world are based on data and reports from the Health Ministry and WHO. The data and report on India’s GDP were obtained from the Ministry of Finance. The data in the segment-by-segment study, which was taken from the regulatory authority website, includes premium collection, growth, accretion, assets, liabilities, market share, and market growth for all forms of insurance. Data has been collected from January 2019 to date in order to compare market growth before and after the COVID19 outbreak.

4.2 Methodology

In India, there are 31 general insurance companies and 24 life insurance companies. Only 26 companies are included in this report, and the rest have been left out due to lack of complete data. A comparative research has been planned to assess the effect of COVID19 on the Indian insurance industry. To demonstrate the statistical significance of the obtained result, bivariate analysis is used and cross-tabulation is applied for comparative analysis. These designs aided in answering questions such as which industry sector experienced accelerated market growth following the pandemic, what is the rate of premium collection before and after COVID19, and which health insurance subcategory showed a significant decrease and increase in premium collection business? COVID19’s effect on India’s top and bottom 10 health retail insurance firms have also been observed.

5 Results

5.1 Product-Wise Industry share

In India, having a motor insurance policy is needed; without it, you would not be able to drive legally. There are two forms of policies in place. Third-party responsibility and a comprehensive plan policy are two of the most important insurance policies. Both plans cover damage to you and your car caused by third parties or natural disasters such as fire, crash, robbery, and others.

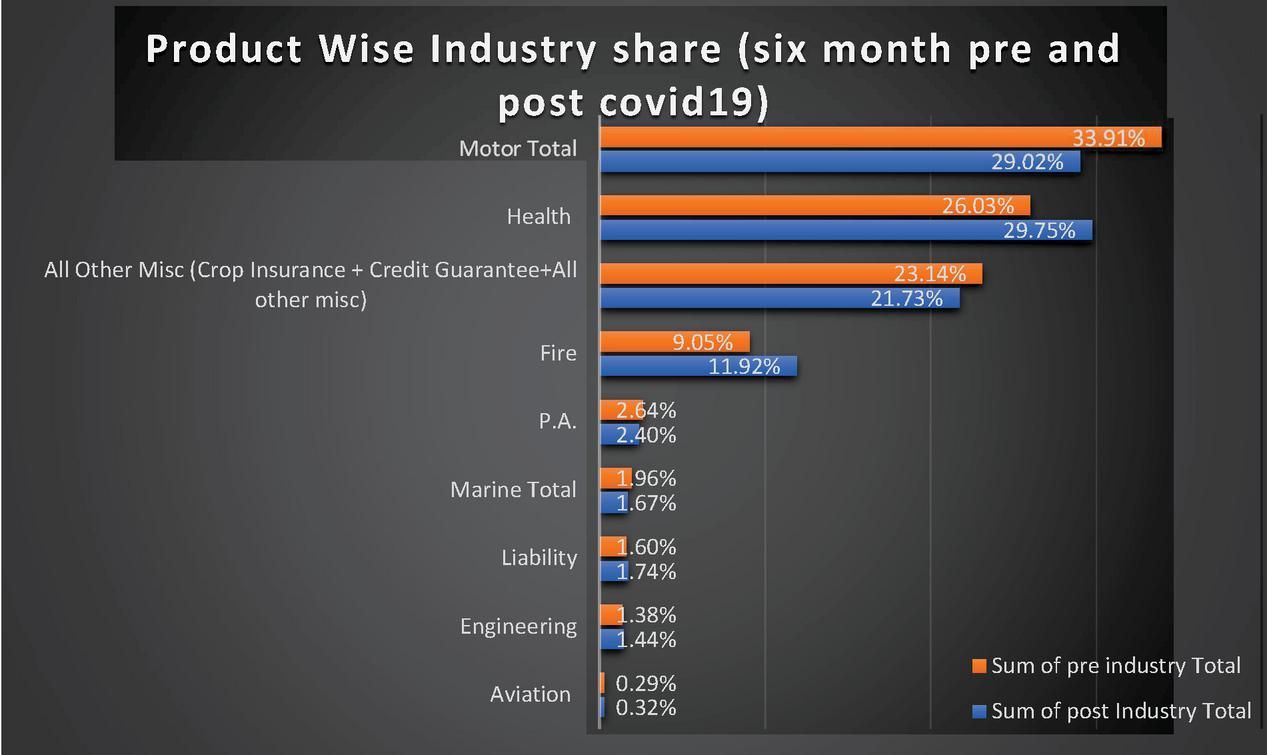

Figure 1 Product-wise industry shares six-month pre and post COVID-19.

Figure 1 show that motor insurance has the highest market share in the insurance industry, accounting for 33.91% of overall premium collections, and that its company deflated to 29.02% after COVID-19. The motor industry experienced a recession prior to COVID-19, and because of the enforced lockdown, the selling of new vehicles came to a halt, resulting in a significant decrease in consumers purchasing new motor insurance policies.

The health insurance industry has benefited from the pandemic. Figure 1 shows that before COVID-19, it collected 26.03% of premium, and after COVID-19, it collected 29.75% of premium, making it the highest premium collecting body in the non-life category. The primary explanation for this is that health insurance covers medical costs such as accidental disease and hospitalisation, annual health check-ups, serious illness, organ donation, maternity benefits, AYUSH, Day-care procedures, and other medical expenses that were not affected by the lockdown but were increased by the pandemic. People seeking to be insured or own a new health insurance policy are looking to be insured or own a new health insurance policy as a result of the pandemic raising medical challenges.

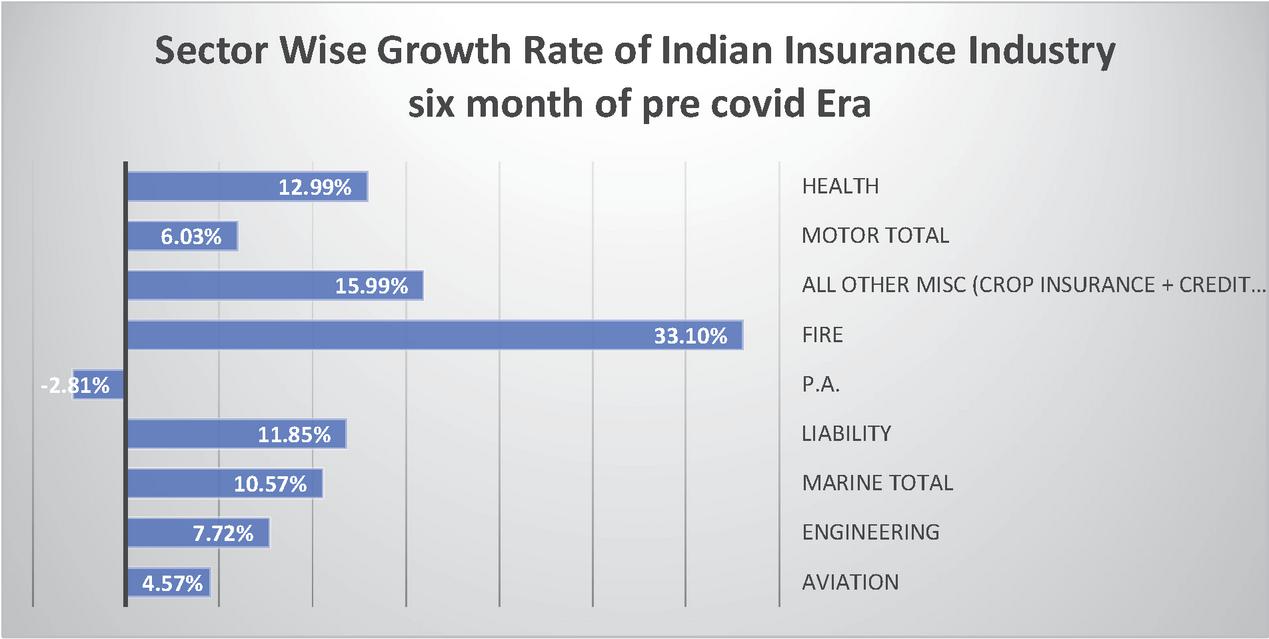

Figure 2a The sector-wise growth rate of the insurance industry six months before covid-19.

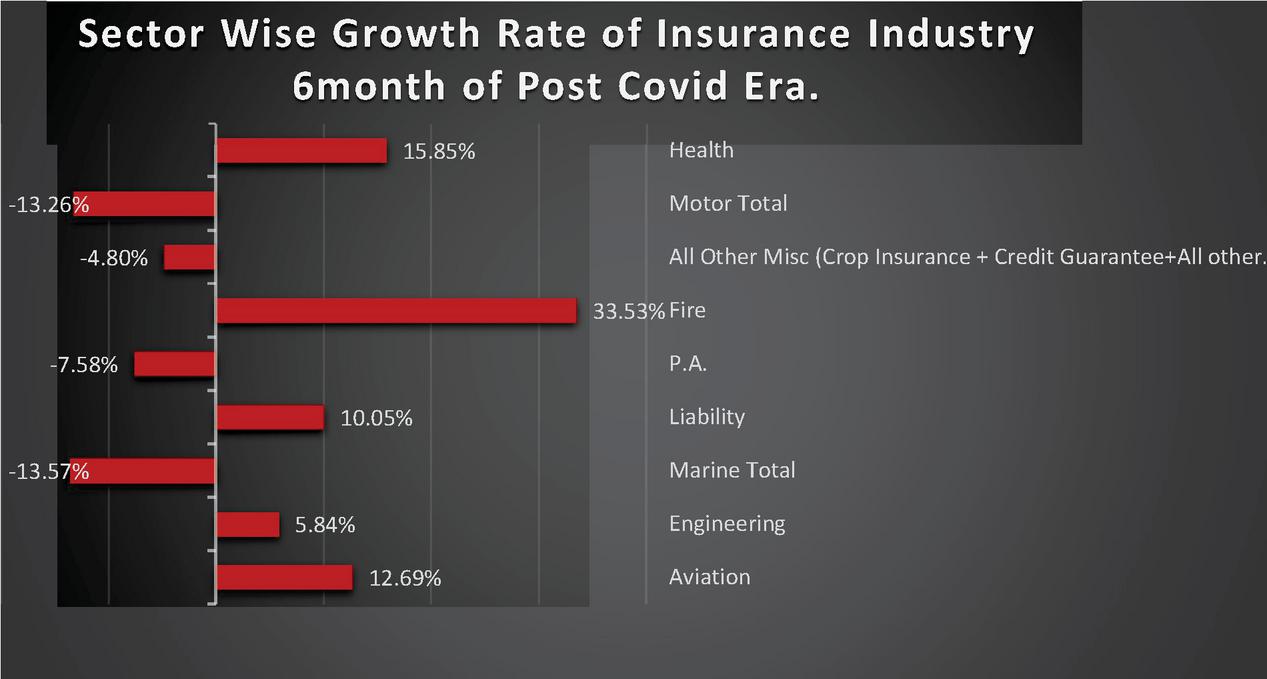

Figure 2b Sector-wise growth rate of insurance industry-six month after covid-19.

5.2 Growth-wise Industry share

COVID-19 has seen a significant shift in the development of the premium series. The first six-month growth rates in each sector before and after COVID-19 are shown in Figures 2a and 2b. As compared to the last six months of the pre-COVID-19 era, the market value of all insurance sectors has decreased since the COVID-19 strike, except for health insurance. Figure 2a shows that, prior to the pandemic, the health insurance business saw a year-over-year increase of 12.99% in premium collection, while the motor insurance business saw a 6.03% increase in premium growth. While Figure 2b shows that since the pandemic, health insurance has been steadily increasing at a rate of 15.85%, motor insurance has been steadily decreasing at a rate of 13.26% during the same time span. Health costs are covered by the health insurance industry. The pandemic has raised the cost of medical and hospitalisation costs, as shown by the company’s expansion.

5.3 Health Insurance Sub-Category

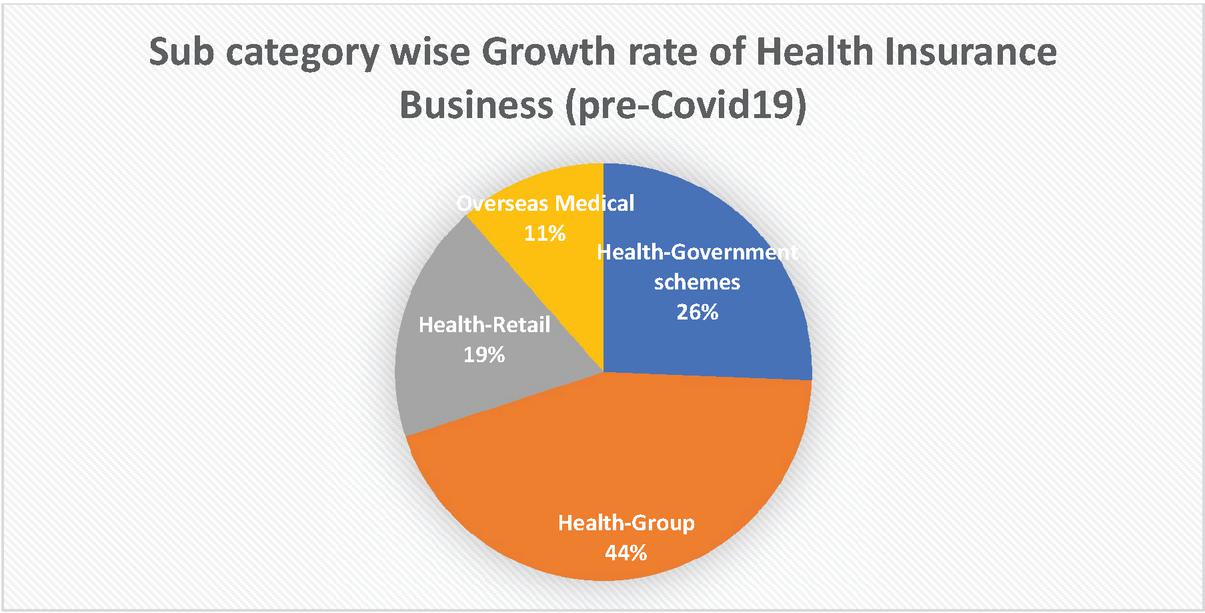

In addition, health insurance has a number of subcategories into which it divides its operations. Overseas Medical, Health-Government Schemes, Health-Group, and Health-Retail are some of the groups. Overseas medical health insurance protects the insured from hospitalization costs incurred outside of India. It encompasses both inpatient (hospitalization) and outpatient (primary medical care) medical experiences.

Figure 3a Subcategory wise growth rate of health insurance business six months before covid19.

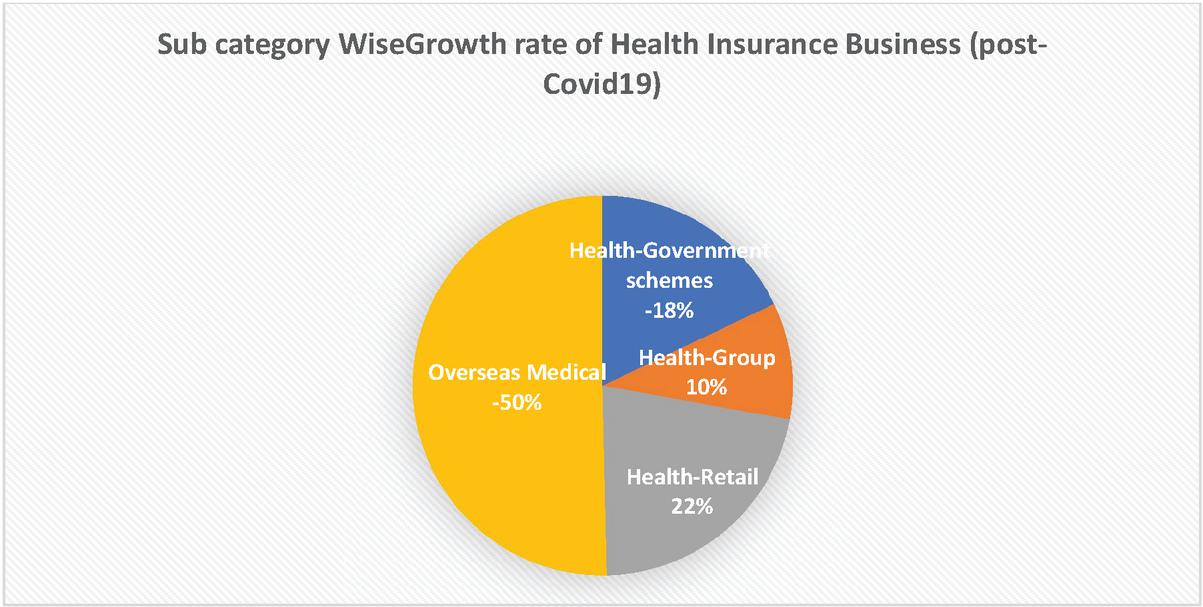

Figure 3b Subcategory wise growth rate of health insurance business six months after covid19.

5.3.1 Sub-category wise growth

Figures 3a and 3b show that premium collection for overseas medical increased by 11% before COVID-19 and then decreased by 50% after the attack. Following the outbreak of COVID-19, all countries seized their borders, preventing the movement of migrants, refugees, international students, travellers, and others. The health-government system premium collection growth rate was 26% before the pandemic, but it fell by 18% afterward. For the poorest members of society, the Indian government has a range of health insurance programmes. According to the National Sample Survey, 86% of rural residents and 81% of city residents were without health insurance. It implies that the majority of Indians are uninsured. The Pradhan Mantri Jan Arogya Yojana is one of several schemes introduced by the Indian government to close this gap. The 107 million poor and uninsured households benefit from this programme, which offers annual health coverage of 5 lakhs per family. Individuals have received 126 million e-cards as part of PM-JAY so far. Even so, almost 1 billion Indians were uninsured, assuming that these 126 million people had no health insurance previously.

Health-group insurance is a form of coverage provided to workers by businesses, housing societies, banks, and employers, with the company paying the premium. Individuals should buy health-retail insurance policies to provide health benefits. Individual policy purchases in the post-pandemic period, however, have changed the market landscape. Figures 3a and 3b show that, in pre-pandemic phase growth, the rate of premium collection of health-groups was 44% and that of health retail was 19%. Individual policy purchases in the post-pandemic period, however, have changed the market landscape. In the post-pandemic phase, the collection of premiums has increased in the health-group by 10% and health-retail by 22% on year-on-year business.

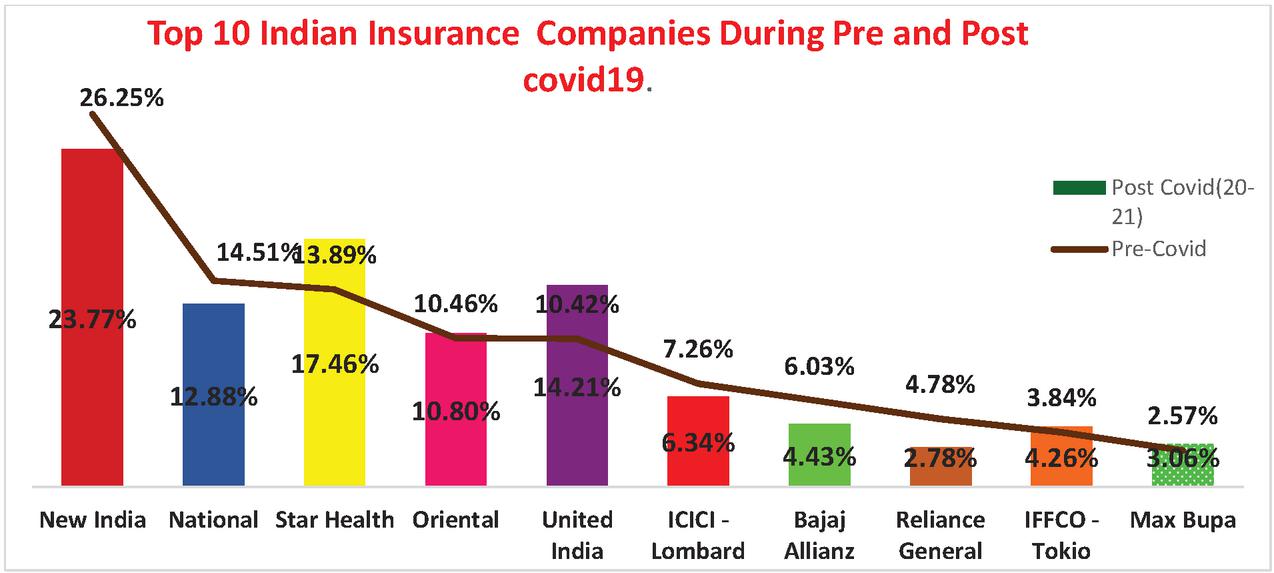

5.3.1.1 The Top 10 Indian Insurance Companies in pre and post COVID-19 period

Even though the health insurance sector grew, not all businesses did. Six of the 26 general insurance companies studied have seen a decrease in premium rise. Figure 4 displays the premium collections of the top 10 Indian insurance firms, showing that New Indian Insurance Firm earned the highest premium of 26.25% in pre-covid19 and 23.75% in post-covid19, with a year-on-year growth rate of just 4.8%.

Figure 4 Shows the top 10 Indian insurance companies in the pre and post COVID-19 period.

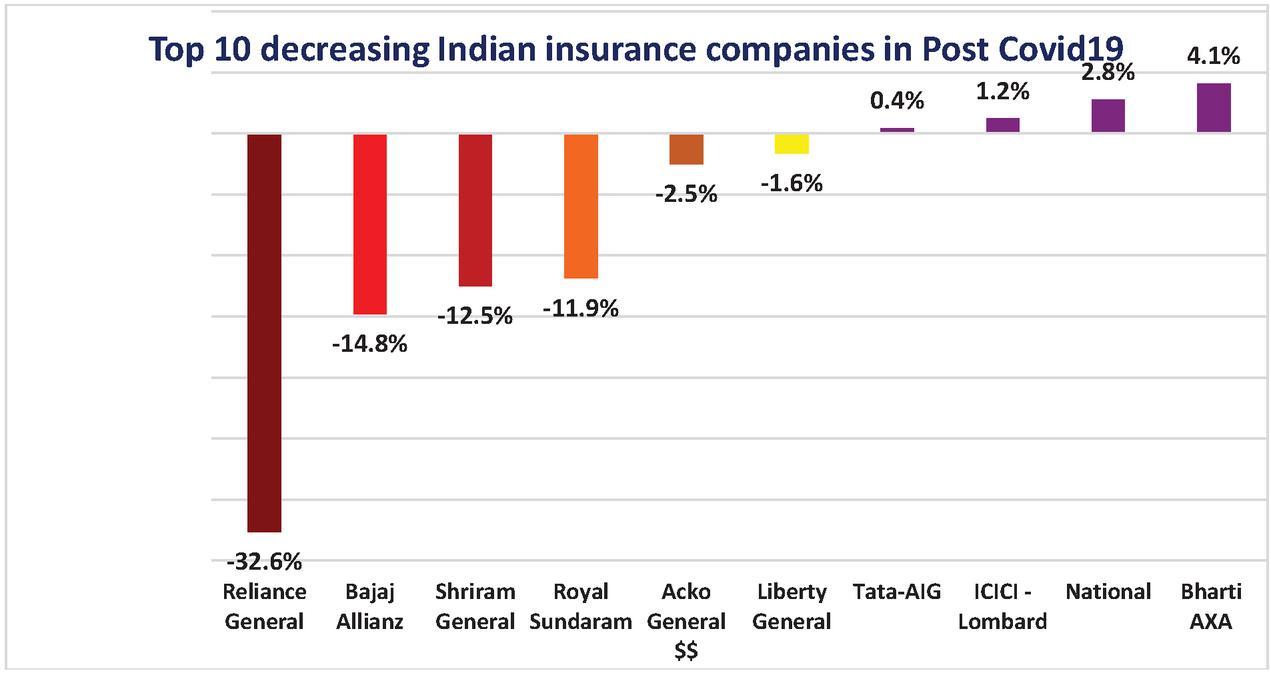

Figure 5 Shows bottom 10 Indian insurance companies’ growth in post-COVID-19.

5.3.1.2 Bottom 10 Indian insurance companies’ growth in post-COVID-19

5.4 Bivariate Analysis

The paired t-test is used to test the efficacy of the premium range of companies in the pandemic. The premium set of 26 companies is shown in Table 1 below before and after. At a 5% level of significance, we consider the null hypothesis that the mean of premium collection before covid19 differs statistically significantly from the mean of premium collection after covid19. Is this premium collection working in the midst of the pandemic? The importance is calculated using SPSS.

Dataset:

Table 1 Data of premium collection of 26 insurance companies

| Insurers | Pre-Covid (six-month) | Post-Covid (six-month) |

| Acko General $$ | 40.06 | 39.05 |

| Bajaj Allianz | 1187.46 | 1011.52 |

| Bharti AXA | 198.09 | 206.17 |

| Cholamandalam MS | 166.9 | 237.57 |

| Edelweiss** | 35.83 | 45.9 |

| Future Generali | 147.59 | 176.21 |

| Go Digit # | 12.92 | 136.54 |

| ICICI – Lombard | 1430.03 | 1447.42 |

| IFFCO – Tokio | 756.46 | 972.17 |

| Kotak Mahindra | 41.77 | 88.04 |

| Liberty General | 136.17 | 133.95 |

| Magma HDI | 21.33 | 38.62 |

| National | 2859.65 | 2939.81 |

| New India | 5173 | 5423.85 |

| Oriental | 2061.1 | 2465.22 |

| Raheja QBE | 0.08 | 0.44 |

| Reliance General | 942.74 | 635.14 |

| Royal Sundaram | 199.61 | 175.89 |

| SBI General | 351.93 | 517.63 |

| Shriram General | 0.48 | 0.42 |

| Tata-AIG | 527.72 | 530.09 |

| United India | 2053.68 | 3242.77 |

| Universal Sompo | 88.03 | 139.31 |

| Aditya Birla | 266.72 | 507.54 |

| Max Bupa | 505.54 | 697.55 |

| Star Health | 2736.77 | 3983.92 |

Test Report:

1. Paired Samples Statistics:

| Mean | N | Std. Deviation | Std. Error Mean | ||

| Pair 1 | Pre-Covid19 | 843.9100 | 26 | 1235.82759 | 242.36573 |

| Post-Covid19 | 992.0285 | 26 | 1427.27165 | 279.91100 |

2. Paired Samples Correlations:

| N | Correlation | Sing. | ||

| Pair 1 | Pre-Covid19 & Post-Covid19 | 26 | 0.977 | 0.000 |

3. Paired Samples Test:

| Paired Differences | |||||||||

| 95% Confidence Interval of the Differences | |||||||||

| Mean | Std. Deviation | Std. Error Mean | Lower | Upper | t | df | Sing. (2-tailed) | ||

| Pair 1 | Pre-Covid19 | 148.11846 | 343.69735 | 67.40460 | 286.94082 | 9.29610 | 2.197 | 25 | 0.0374713 |

| Post-Covid19 | |||||||||

According to the above analysis, the pre-COVID-19 and post-COVID-19 individual means are 843.9100 and 992.0285 respectively, their standard deviations are 1235.82759 and 1427.27165, and the standard error means are 242.36573 and 279.91100, respectively. The set of premiums in the pre-COVID-19 and post-COVID-19 periods was strongly positively correlated, according to paired sample correlation. The mean difference is 148.11846, the standard deviation is 343.69735, the standard error is 67.40460, and the t-statistic is 2.197, according to paired sample test results. The test rejects the null hypothesis with a significant value of 0.0374713, which is less than 0.05, and all the values are within the 95% confidence interval mean. The test rejects the null hypothesis with a significant value of 0.0374713, which is less than 0.05, since all of the values are inside the 95% confidence interval mean. As a result, our test is statistically valid, and the mean premium collection before COVID-19 differs from the mean premium collection after COVID-19 in a statistically significant way.

6 Discussion and Conclusion

The insurance sector saw both a surge and a drop in business during the pandemic. Insurances such as motor, marine, fire, house insurance, travel insurance, airlines insurance, and so on are seeing a significant drop in business, while health insurance is experiencing both an increase and a decrease in business. The number of claims has grown in the health insurance industry, resulting in a decrease in cash flow, but the number of new clients who have acquired insurance has climbed, indicating company growth.

It can be observed from the analysis that the health insurance industry has benefited from increased public awareness of health problems as a result of the pandemic, whereas the stagnant motor insurance sector has seen a severe drop. It’s feasible that the insurance business should plan forward for the future. A corporate continuity strategy, an employee safety and well-being plan, crisis management task forces, cash, and capital flow during a crisis, maintaining in touch with stakeholders, and cybersecurity are all important aspects of operating a corporation successfully.

The effect of COVID-19 on the insurance industry is fascinating to investigate because it not only taught society how to thrive in a pandemic situation, but it also suggested tactics that should be pursued in the future to prevent such market uncertainty.

References

(COVID-19), W. C. (2020). WHO Coronavirus (COVID-19) Dashboard. Retrieved September 21, 2020, from https://covid19.who.int/

Babuna, P., Yang, X., Gyilbag, A., Awudi, D. A., Ngmenbelle, D., & Bian, D. (2020, August 10). The Impact of COVID-19 on the Insurance Industry. International journal of environmental research and public health, 17, 5766. doi:10.3390/ijerph17165766

Brand India. (2020). Retrieved November 25, 2020, from IBEF: https://www.ibef.org/industry/insurance-sector-india.aspx

CII. (2020). Manufacturing. Retrieved December 25, 2020, from Confedration of Indian Industry: https://www.cii.in/sectors.aspx?enc=prvePUj2bdMtgTmvPwvisYH+5EnGjyGXO9hLECvTuNsfVm32+poFSr33jmZ/rN+5

Dhoot, V. (2020, November 28). Q2 manufacturing rebound puzzles economists. Retrieved December 25, 2020, from The Hindu: https://www.thehindu.com/business/Economy/q2-manufacturing-rebound-puzzles-economists/article33201994.ece

Director-General, W. (2020, March 11). WHO Director-General’s opening remarks at the media briefing on COVID-19 – 11 March 2020. Retrieved September 21, 2020, from https://www.who.int/director-general/speeches/detail/who-director-general-s-opening-remarks-at-the-media-briefing-on-covid-19---11-march-2020

ET. (2020, 02 September). GDP growth at 23.9% in Q1; first contraction in more than 40 years. Retrieved November 30, 2020, from The Economic Times: https://economictimes.indiatimes.com/news/economy/indicators/gdp-growth-at-23-9-in-q1-worst-economic-contraction-on-record/articleshow/77851891.cms

IBEF. (2020). Brand India. Retrieved November 11, 2020, from IBEF: https://www.ibef.org/industry/insurance-sector-india.aspx

IBEF. (2020). Brand India. Retrieved December 25, 2020, from IBEF: https://www.ibef.org/industry/services.aspx

IMF. (2020, June 01). World economic Outlook UPDATE June 2020:A crisis like no other, an Uncertain Recovery. World economic Outlook . Retrieved jan 11, 2020, from IMF: https://www.imf.org/en/Publications/WEO/Issues/2020/06/24/WEOUpdateJune2020

Industry Performance . (2020). Retrieved from General Insurance Council: http://www.gicouncil.in/statistics/industry-statistics/segment-wise-report-on-homepage/

IRDA. (2020, July 31). History of insurance in India. Retrieved from IRDA: https://www.irdai.gov.in/ADMINCMS/cms/NormalData_Layout.aspx?page=PageNo4&mid=2

Jaipuria, S., Parida, R., & Ray, P. (2020). The impact of COVID-19 on tourism sector in India. Tourism Recreation Research, 0250-8281. doi: 10.1080/02508281.2020.1846971

Kumar, D. (2020). COVID-19 India Timeline. Retrieved September 22, 2020, from The Wire: https://thewire.in/covid-19-india-timeline

Mallapur, C. (2020, October 15). Here’s How COVID-19 Has Hurt The Indian Aviation Industry. Retrieved December 25, 2020, from Moneycontrol: https://www.moneycontrol.com/news/business/economy/heres-how-covid-19-has-hurt-the-indian-aviation-industry-5965511.html

Monthly Business – Life. (2020). Retrieved from IRDAI: https://www. irdai.gov.in/ADMINCMS/cms/frmGeneral_List.aspx?DF=MBFL&mid=3.1.8

Roy, J. (2020). COVID-19: Impact on the Indian insurance industry. PwC, Insurance Digital Assests and Leader. Delhi, India: PwC. Retrieved from https://www.pwc.in/assets/pdfs/services/crisis-management/covid-19/covid-19-impact-on-the-indian-insurance-industry.pdf

Shekhar, R., & Pandey, S. (2020, May 06). “Adjusting to the New Normal” Impact of COVID-19 in Insurance Industry. NATIONAL WEBINAR ON COVID 19 “Changing Dynamics Around The Globe”. doi: 10.13140/RG.2.2.20492.33922

Web-Desk, E. (2020, November 27). India GDP Q2 Data: India’s GDP contracts 7.5% in Q2, enters technical recession. Retrieved December 12, 2020, from The Indian Express.

Wikipedia. (2020, March 02). Economic impact of the COVID-19 pandemic in India. Retrieved November 25, 2020, from Wikipedia: https://en.wikipedia.org/wiki/Economic_impact_of_the_COVID-19_pandemic_in_India

Winck, B. (2020, April 18). The IMF says its forecast for the COVID-19 recession might now be too optimistic. Retrieved January 12, 2020, from World Economic Forum: https://www.weforum.org/agenda/2020/04/imf-economy-coronavirus-covid-19-recession/

Biographies

Anjali is a student of post-graduation in Statistics and Data Analytics at Lovely Professional University, Punjab, India. She has completed her graduation in Mathematics (Hons) with 71.8% marks from BR Ambedkar Bihar University and Post-Graduation with 8.72 CGPA from LPU

Geeta Arora is an Associate Professor in the Department of Mathematics at Lovely Professional University, Punjab, India. She has her M.Sc. degree in Mathematics from Gurukul University, Haridwar and Ph.D. degree in Mathematics from the IIT Roorkee, India. She has over nine years of teaching experience and has published around 30 research papers with eight book chapters in both international and national Journals. Her area of research is development of numerical methods and is currently working in the field of Statistics.

Journal of Graphic Era University, Vol. 9_2, 195–214.

doi: 10.13052/jgeu0975-1416.926

© 2021 River Publishers